USDA Wheat Baseline, 2010-19

Each year, USDA updates its 10-year projections of supply

and utilization for major field crops grown in the United

States, including wheat (see Overview

of the USDA Baseline Process for more information).

One key use of the projections is as a "baseline" from

which to analyze the impacts of potential policy changes

affecting U.S. agriculture.

This discussion summarizes analysis underlying the wheat

projections for 2010-19. Details about projections for

the U.S. macroeconomy, other U.S. crops, U.S. livestock,

farm income and food prices, and U.S. and global agricultural

trade, which are critical components of this analysis,

can be found in the Agricultural

Baseline Projections briefing room.

The U.S. wheat sector faces many long-term challenges.

- The long-term projections point to a smaller U.S.

wheat planted area compared to recent years, a continuation

of a long-term trend as profitability relative to other

crops, particularly corn and soybeans, has declined.

- The sharp decline in domestic food use of wheat since

2000—arising from changing consumer preferences—appears

to have ended with future growth likely to be limited

to population growth.

- Internationally, in addition to traditional global

competitors (Canada, Argentina, Australia, and the European

Union), Ukraine and Russia have emerged as new competitors

with the United States in foreign markets in years when

their production is high. The overall result in the

projections is a smaller U.S. share of an expanding

world wheat trade market.

The discussion is divided into five sections:

Supply Background

Several long-term factors play important roles in the

downward trend of the U.S. wheat crop during 2010-19.

Nonetheless, the United States remains a major wheat-producing

country, with output exceeded only by China, the European

Union (EU-27), and India. In the United States, wheat

ranks third among field crops in both planted acreage

and value of production, behind corn and soybeans.

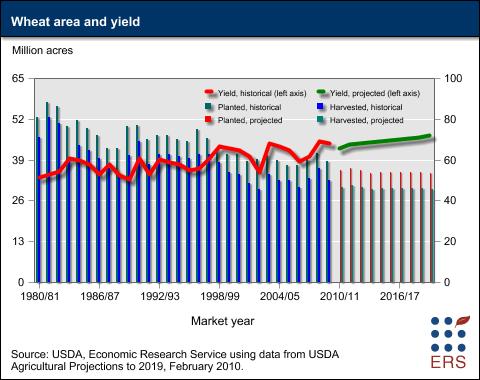

U.S. wheat planted area has trended down for many

years. U.S. wheat area has varied widely during the

past half-century, peaking in the early 1980s. Wheat area

dropped off sharply in the mid 1980s, primarily due to

relatively large Acreage

Reduction Program (ARP) levels implemented when Government-owned

stocks were very large. By 1987-88, nearly 30 percent

of the national wheat base acreage had been idled by farmers

participating in this voluntary program in order to be

eligible for commodity nonrecourse

loans and deficiency

payments. Wheat area recovered in the late 1980s through

mid-1990s as stocks declined and prices rose, thus lessening

the need for ARPs. ARPs were eliminated under 1996 Farm

Act, starting with the 1996 crop.

d d

Get this chart as a JPG

or a PNG.

The introduction of full planting flexibility in the

1996 Farm

Act enabled farmers to switch to alternative crops or to idle

their land without affecting program benefits. Planting

flexibility increased competition for area among corn,

oilseeds, and wheat, which put downward pressure on U.S.

wheat acreage. Planted wheat area in the United States

is down by about 30 percent from an average of 85 million

acres in the early 1980s to an average of 59.6 million

acres over the past 5 years.

enabled farmers to switch to alternative crops or to idle

their land without affecting program benefits. Planting

flexibility increased competition for area among corn,

oilseeds, and wheat, which put downward pressure on U.S.

wheat acreage. Planted wheat area in the United States

is down by about 30 percent from an average of 85 million

acres in the early 1980s to an average of 59.6 million

acres over the past 5 years.

Wheat land switched to other uses. Wheat area

has dropped off in the United States as farmers have taken

their land out of production or switched to alternative

crops offering higher returns. Enrollment in the Conservation

Reserve Program (CRP) is concentrated in those regions

where wheat production predominates. About 60 percent

of the land enrolled in the CRP is located in the Plains

States, stretching from Texas to North Dakota and Montana.

USDA estimates that about 8 million acres of CRP land

had been planted to wheat or in a wheat-fallow rotation

prior to enrollment.

In the traditional wheat growing areas of the Plains

there is a longer-than-30-year trend to reduce area fallowed

by planting alternative crops and lengthening crop rotations.

One of the factors facilitating the planting of alternative

crops, corn and sorghum, for example, is the increased

use of reduced-till and no-till to increase water storage

in the soil allowing for improved yields of these crops.

For example, in western Kansas, the historical wheat/fallow

rotation has been most commonly replaced by a rotation

of wheat/grain sorghum/fallow in which wheat is planted

1 year out of 3 instead of 1 year out of 2. Though cropping

intensity increases, wheat is planted less frequently.

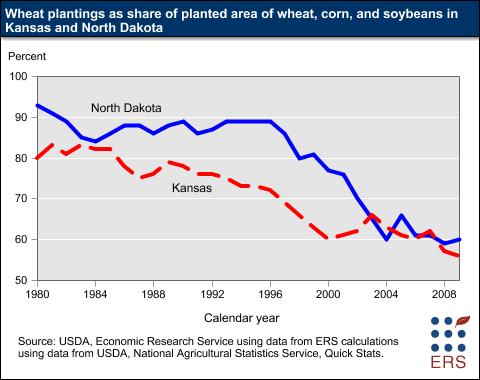

The trend of planting more corn and soybeans on acreage

traditionally planted to wheat can be illustrated by examining

data for Kansas and North Dakota, two of the country's

largest wheat-producing States. In the early 1980s, wheat

accounted for 80-90 percent of the total wheat, corn,

and soybeans planted in Kansas and North Dakota. In recent

years, wheat's share has dropped to 56-62 percent of the

total.

d d

Get this chart as a JPG

or a PNG.

Genetic gains for competing crops on the Plains.

Loss of wheat acreage to row crops, such as corn and soybeans,

on the Plains reflects strong genetic improvements in

those alternative crops. New varieties of corn and soybeans

can be planted farther west and north in areas with drier

conditions or shorter growing seasons. Plus, weed control

is far easier with the development of herbicide-resistant

varieties (see the Agricultural

Biotechnology briefing room for more information).

The pace of genetic improvement has been slower for wheat

than for some other field crops, resulting in little growth

in wheat yields, which makes wheat a less attractive cropping

option for farmers. Genetic improvement for wheat has

been slower because of genetic complexity and because

of lower potential returns to commercial seed companies,

factors that discourage investment in research. For instance,

farmers have to buy seed corn each year because seed saved

from a hybrid cannot be used for a subsequent crop. This

creates a large annual market for seed companies and the

returns to investment needed to finance breeding programs

to develop improved varieties. In contrast, many wheat

farmers, particularly in the Plains States, use saved

seed from the previous year's crop instead of buying from

dealers every year because the wheat varieties grown in

the United States are not hybrids. This practice sharply

reduces the potential market for branded commercial seed

wheat and, thus, investment in seed development research.

d d

Get this chart as a JPG

or a PNG.

Wheat disease also a factor. Concerns about wheat

disease problems in the Northern Plains, particularly

scab (head blight) in North Dakota and Minnesota, influenced

planting decisions starting in the 1990s and will do so

in the future. The increased incidence of this disease

may stem in part from larger corn plantings and reduced

tillage practices in traditional wheat areas in the Northern

Plains. Both activities provide hosts for disease organisms.

Ethanol expansion in the United States. A large

expansion in ethanol production has taken place in the

United States, which has affected virtually every aspect

of the field crops sector, ranging from domestic crop

utilization and exports to prices and the allocation of

acreage among crops. Cellulosic sources of feedstocks

for ethanol production hold some promise for the future,

but the primary feedstock in the United States is currently

corn. Market adjustments to this increased corn demand

extend well beyond the corn industry. In particular, this

has raised corn area and contributed to declines in wheat

area. Many aspects of the livestock sector are affected

too, including the substitution of ethanol byproduct feedstuffs

for corn and other feeds in rations.

Demand Background

Just as U.S. wheat production faces pressures from multiple

factors, several domestic and international market factors

underlie long-term developments for U.S. wheat demand

during 2010-19.

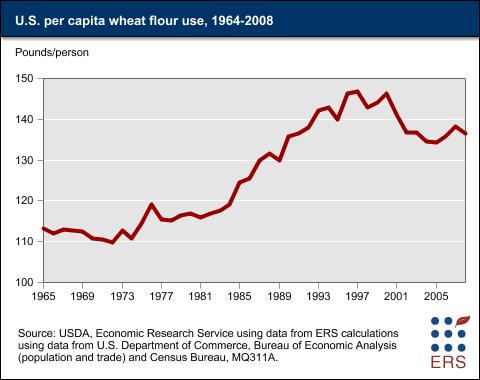

Decline in per capita flour use slows. Domestic

per capita wheat flour use for calendar year 2008 is estimated

at 136.6 pounds, 1.7 pounds below the 2007 estimate. Flour

use rose in 2006 and 2007 from the recent low of 134.4

pounds in 2005. This 2005 low was reached after the sharp

declines in per capita use from 146.3 pounds in 2000.

Until the late 1990s, U.S. wheat producers could count

on rising per capita food use of wheat to expand the domestic

market for their crop. The strength of this domestic market

developed out of the historic turnaround in U.S. per capita

wheat use that occurred in the early 1970s.

d d

Get this chart as a JPG

or a PNG.

For nearly 100 years, per capita wheat use had declined

in the United States, as strenuous physical labor became

less common and diets became more diversified. Wheat use

dropped from over 225 pounds per person in 1879 to a low

of 110 pounds in 1972. By 1996, use had rebounded to 146.8

pounds per capita. The overall growth in per capita use

that occurred between 1973 and 1997 reflected changes

that included the boom in away-from-home eating, the desire

of consumers for greater variety and more convenience

in food products, promotion of wheat flour and pasta products

by industry organizations, and wider recognition of health

benefits stemming from eating high-fiber, grain-based

foods.

This growth ended in 1997 due to changing consumer preferences,

including more weight-conscious people following diets

with fewer carbohydrates. Consumer interest in these diets

spiked in 2000. The sharp drop in per capita flour use

that began in 2000 seems to have ended.

Feed use varies. Feed use of wheat varies with

price and crop quality. Feeding wheat to livestock increases

when the price premium between wheat and corn is narrow,

which typically occurs in the summer after winter wheat

is harvested, but before corn is harvested. Wheat feeding

also increases when wheat quality is impaired, reducing

its value relative to corn. For example, when there is

excessive rainfall at harvest time, some wheat varieties

are susceptible to preharvest sprouting. When sprouting

occurs, biochemical changes in the wheat kernel diminish

baking qualities for food products, making the wheat suitable

only as a low quality livestock feed.

U.S. exports down from recent peak. Projected

2009/10 exports, at 875 million bushels, are down 140

million bushels from 2008/09 and down 388 million bushels

from 2007/08. Exports in 2007/08 were at a 15-year high

as adverse weather around the world reduced global production

and increased the demand for U.S. wheat. Farmers in many

countries responded to the high prices that resulted from

the tightest global stocks-to-use situation in 30 years,

and the resulting additional supplies steadily reduced

the demand for relatively higher-priced U.S. wheat.

World market evolves. Longer term, growing global

demand for wheat imports is concentrated in those developing

countries where robust income and population growth underpin

increases in demand. Such markets include Sub-Saharan

Africa, Egypt, Pakistan, Algeria, Indonesia, the Philippines,

and Brazil.

Ukraine, Russia, and Kazakhstan have become significant

wheat exporters in recent years, together surpassing U.S.

exports in 2008/09. These countries were net importers

as recently as 1995. Low costs of production and new investment

in their agricultural sectors have enabled their world

market share to climb despite the region's highly variable

weather and production. During the mid- to late-1990s,

their combined share of world exports was less than 5

percent, averaging less than million metric tons (mmt).

Toward the end of the 2000s, their share of world exports

had risen to nearly 20 percent and for 2007 and 2008 exports

averaged nearly 22.5 mmt. For comparison, the U.S. share

of world exports fluctuated up and down between 20 percent

and 30 percent.

Projections for U.S. Wheat Supply

and Use

The long-term projections for U.S.

wheat for 2010-19 were heavily influenced by prospects for increased

foreign competition and wheat's slow yield gains as both

contribute to lower relative profitability compared with

other domestic crops and lower domestic wheat area.

for 2010-19 were heavily influenced by prospects for increased

foreign competition and wheat's slow yield gains as both

contribute to lower relative profitability compared with

other domestic crops and lower domestic wheat area.

Wheat yields continue slowly rising. Yields for

2011 and beyond are national all-wheat trend-yields using

1985-2009 data. The assumed annual increase averages 0.35

bushels per acre over the projection period. For comparison,

corn and soybean annual trend-yield gains are projected

at 2 bushels per acre and 0.4 bushels per acre, respectively.

The yield assumption for 2010 is 42.7 bushels per acre,

which is below the national all-wheat trend yield. This

yield was projected using trends by type of wheat, adjusted

for specific 2010 information. The 2010 trend-yield estimates

for durum and other spring wheat did not include 2009

because 2009 growing season weather in the Northern Plains

was unusually favorable for wheat and resulted in markedly

higher yields than trend. The trend-yield estimate for

winter wheat includes 2009, but was adjusted to account

for prevented plantings in the soft red winter (SRW) areas.

Excessive rainfall delayed the fall row crop harvest,

especially in the SRW areas, therefore, preventing timely

winter wheat seeding. The all-winter-wheat trend yield

is adjusted downward to account for the lower expected

SRW area. SRW yields are typically higher than the average

for all-winter wheat because of more abundant moisture.

Wheat plantings expected to be fall with weak demand

over the next decade. Wheat plantings are

projected down in 2010 with relatively low prices at planting

and expected prevented plantings. Area then rebounds in

2011, the second year of the projections, with a normal

fall planting season. Planted area is then expected to

fall to a low of 53.5 million acres in 2013. With relatively

weak overall demand growth and continuing large stocks,

producer returns remain lower than in recent years.

d d

Get this chart as a JPG

or a PNG.

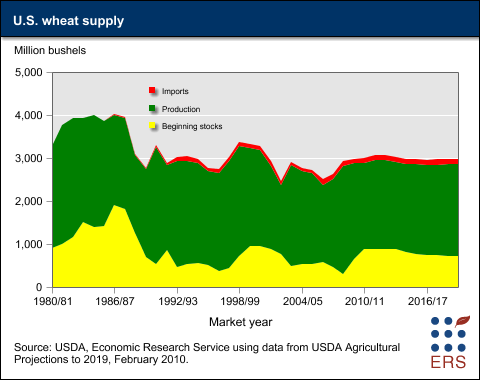

Wheat production is expected to expand slightly with

rising yields. Projected production rises in 2011

and then falls through 2013, when the planted area low

of 53.5 million occurs. Production then rises unevenly

with the increasing yields. Imports of wheat are expected

to remain relatively small, but increase slowly, adding

to U.S. supplies. However, beginning stocks are expected

to drift slowly down over the period. The result is that

U.S. wheat supplies are projected to fluctuate over the

10-year projections period with a slight downward trend.

d d

Get this chart as a JPG

or a PNG.

Total use of wheat is projected to rise slowly.Total

use of U.S. wheat rises slowly over the next decade, mostly

due to gains in projected food use. Foreign demand for

U.S. wheat is expected to be limited to 900 million bushels

annually for most of the period. U.S. exports face increased

global competition, especially from the former Soviet

Union countries. Russia’s exports alone are projected

to surpass U.S. exports by 2016/17 and, by the end of

the 10-year period, are projected to exceed U.S. exports

by more than 150 million bushels. The U.S. share of world

wheat trade is projected to decline from 19.1 percent

to 16.4 percent over the

10-year period.

d d

Get this chart as a JPG

or a PNG.

Wheat food use increases slowly. Per capita food

use of wheat in the United States has fallen sharply in

recent years, but this decline is projected to end in

the longer term. Total projected food use at the start

of the projection period is adjusted downward to reflect

a higher than average flour extraction rates for the 2009

crop. A high extraction rate means that fewer bushels

of wheat need to be milled to produce a given quantity

of flour. After some rebound due to an assumed return

to an average extraction rate, long-term annual growth

is 9 million bushels to the end of the projection period.

This growth in total food use reflects assumptions of

1) slowing annual population growth from 0.93 percent

to 0.86 percent, 2) constant per capita use, and 3) a

long-term average flour extraction rate.

Prices and stocks decline, but remain historically

high. Wheat prices are down from the recent spike

to the record $6.78 per bushel in 2008/09, but remain

historically high at $4.75 per bushel at the end of the

period. Stocks slowly decline from the current high levels,

but are still above 700 million bushels at the end of

the projections. For comparison, in 2007/08 the U.S. ending

stocks were only 306 million bushels, the lowest since

the mid-1940s.

Projections for World Wheat

Trade

The USDA baseline also provides projections for global

trends in wheat trade. The following discussion on wheat

trade is from the Global

Agricultural Trade chapter of the Agricultural

Baseline Projections briefing room.

World Wheat Imports. Growth in wheat

imports is concentrated in those developing countries

where income and population gains drive increases in demand.

The largest growth markets include Sub-Saharan Africa,

Egypt, Algeria, other countries in the Africa and Middle

East region, Pakistan, and Indonesia. World wheat trade

(including flour) expands by 25 million tons (20 percent)

between 2010 and 2019 to more than 149 million tons.

- Egypt maintains its position as the world's largest

wheat importing country, as its imports climb slowly

to more than 11 million tons. Imports by the EU,

Algeria, Brazil, and Indonesia are each projected to

exceed 6 million tons by 2019.

- Imports by developing countries in Africa and the

Middle East rise 13.2 million tons and account for more

than 50 percent of the total increase in world wheat

trade. Saudi Arabia has adopted a policy to phase out

wheat production by 2016 because of water scarcity concerns,

and imports are projected to rise to more than 3 million

tons by 2019. China’s per capita consumption of wheat

is expected to continue to decline.

- In most developing countries, almost no change in

per capita wheat consumption is expected, but imports

are projected to expand modestly because of population

growth and limited potential to expand production. Rising

per capita consumption of wheat in Indonesia, Vietnam,

and some other Asian countries, reflects a dietary shift

from rice as incomes rise. Nonetheless, overall global

per capita wheat consumption is projected to decline

slightly during the coming decade.

- Lower wheat-to-corn price ratios during most of the

projection period enable wheat to compete effectively

with corn for feed use in a number of countries. Europe

is expected to continue to account for about half of

global wheat feeding.

d d

Get this chart as a JPG

or a

PNG

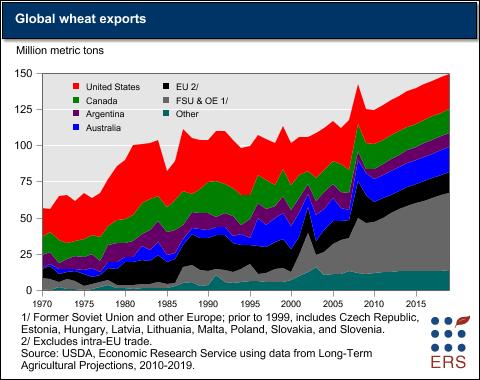

World wheat exports. The traditional

5 largest wheat-exporting nations (the United States,

Australia, the EU, Argentina, and Canada) are expected

to account for 55 percent of world trade in 2019, compared

with roughly 70 percent during the last 5 years. This

decrease in share is mostly due to increased exports from

the Black Sea area. U.S. wheat exports are projected to

account for less than 17 percent of global wheat trade

at the end of the projection period, down from about 25

percent in the past 5 years. Although world wheat stocks

are projected to continue increasing from their 2007 lows

during the next several years, prices are projected to

remain above their pre-2006 average levels.

- The shares of the world wheat market decline for Canada,

the United States, the EU, and Australia, while shares

increase for Russia, Ukraine, Kazakhstan, Argentina,

and China.

- Russia, Ukraine, and Kazakhstan have become significant

wheat exporters in recent years. Low costs of production,

new investments in agriculture, and generally favorable

weather since 2001 have enabled their combined share

of global wheat trade to climb to about 22 percent during

the last 3 years. Although Russia is expected to continue

increasing wheat production for domestic feed use, exports

from the FSU are projected to continue gaining market

share, and to account for about 35 percent of world

exports by 2019. However, because of the region’s highly

variable weather and yields, year-to-year volatility

in production and trade can be expected.

- EU wheat exports decline through 2012 as more wheat

is used for ethanol. EU exports then rise slowly during

the later years of the projection period, reaching 14

million

tons in 2019.

- In Canada, increased demand for vegetable oils (especially

rapeseed oil) and for barley is expected to reduce wheat

area and limit any growth in wheat exports.

- Wheat exports by Turkey and other smaller exporters

change little or trend slowly downward during the projection

period.

d d

Get this chart as a JPG

or a PNG.

Market Forces Constraints Future

Growth in U.S. Wheat Sector

The U.S. wheat sector is facing long-term challenges

as productivity gains and returns for competing field

crops outpace those for wheat. Over the next 10 years,

U.S. wheat planted area is projected to fall sharply from

the recent high in 2008/09. Wheat yield improvements are

expected to continue lagging those for competing row crops,

primarily corn and soybeans. U.S. exports are expected

to stagnate with the increased global competition, particularly

from Russia, Ukraine, and Kazakhstan. Furthermore, domestic

food use, while growing, no longer provides the dynamic

market growth experienced in the 1970s through the mid-1990s.

Consequently, farmers will focus on other crops, such

as corn and soybeans, because of low relative returns

to wheat.

|

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}